Technology

Profit Recovery in France and Germany Faces Challenges Ahead

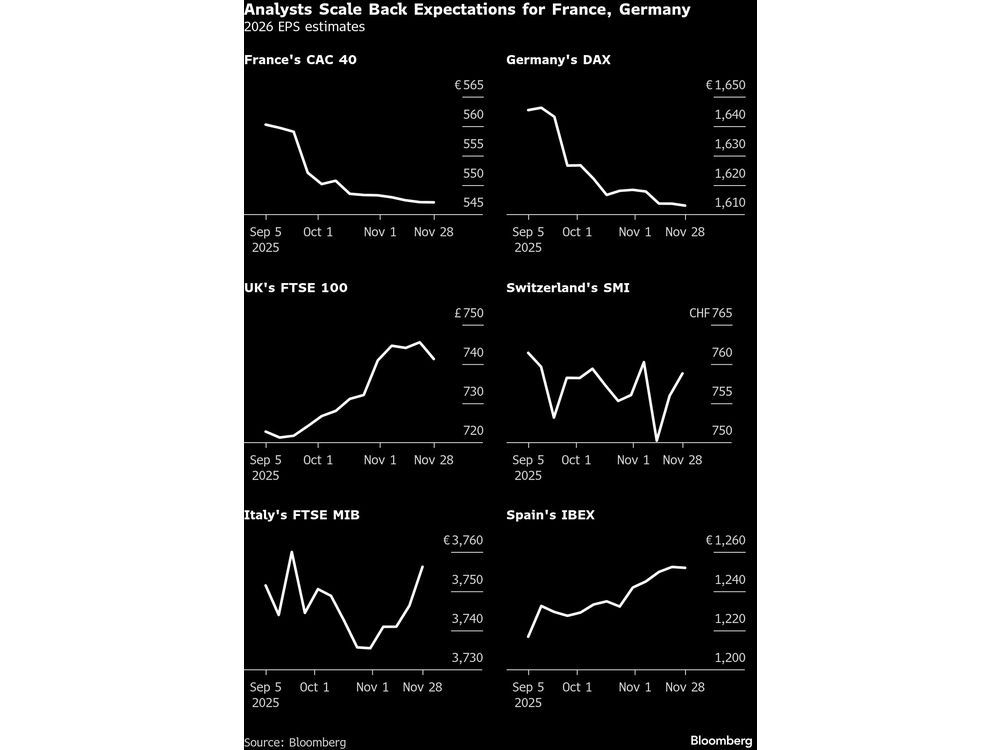

Profit expectations for France and Germany are under pressure as the luxury and automotive sectors encounter significant challenges. Recent data from Bloomberg Intelligence indicates a downward revision of earnings forecasts for France’s CAC 40 and Germany’s DAX indexes for the upcoming year. In contrast, estimates for other European benchmarks are being adjusted upwards, highlighting a divergence in market performance.

The CAC 40 and DAX indexes are heavily weighted towards consumer discretionary and industrial sectors. This reliance raises concerns, particularly as both sectors may struggle to meet elevated expectations in 2024. The DAX, for instance, is largely comprised of major automotive manufacturers such as BMW AG, Volkswagen AG, and Mercedes-Benz Group AG, all of which have faced multifaceted challenges this year.

Luxury Sector Recovery Uncertain

In France, leading luxury brands like LVMH Moët Hennessy Louis Vuitton SE, Hermès International SCA, and Kering SA are tasked with demonstrating that demand recovery, particularly in the United States and China, is not only ongoing but also strengthening. Kering is especially under scrutiny, as its shares have surged by 23% this year, fueled by optimism surrounding new Chief Executive Officer Luca de Meo. Analyst Adam Cochrane from Deutsche Bank cautions that while investor sentiment is currently positive, there is a risk that expectations for the company’s performance could become overly ambitious. He predicts potential earnings downgrades when Kering reveals its strategic plans in early 2024.

Automotive Sector Faces Structural Challenges

Germany’s automotive sector is grappling with various pressures, including US tariffs and a slowdown in demand from China. The competitive landscape has intensified with increasing pressure from Chinese car manufacturers, further complicating recovery efforts. According to analysts Kaidi Meng and Laurent Douillet from Bloomberg Intelligence, the DAX’s ability to rebound is significantly tied to the automotive industry, which continues to face structural issues despite any cyclical improvement in demand.

Analyst Harald Hendrikse from Citigroup warns of persistent declines in market share and profitability for European carmakers in China, which are expected to persist through 2026. The exposure of BMW and Mercedes to the Chinese market places them at heightened risk of marked earnings declines.

On the industrial front, the outlook for German manufacturers depends heavily on substantial infrastructure investments and increased defense spending within the European Union. While a softer euro and geopolitical stability could provide support, these advantages are not guaranteed. Industrial firms like Daimler Truck Holding AG are particularly vulnerable, facing a 25% tariff on medium- and heavy-duty trucks sold in the US, which could potentially reduce their profits by up to 30%.

French industrial companies, including Schneider Electric SE and major defense players such as Safran SA and Airbus SE, may benefit from burgeoning markets driven by data-center expansion, heightened defense spending, and the energy transition. Nevertheless, political uncertainty continues to cast a shadow on expectations, complicating any prospects for a major recovery.

As 2026 approaches, both French and German stocks are positioned with a “fragile outlook,” according to Bloomberg Intelligence. Factors such as “stretched valuations, uneven earnings momentum, and mounting fiscal pressure” pose challenges that could hinder the anticipated profit rebound in these two major European economies.

iShares Core Dividend Growth ETF Faces Challenges; Alternatives Suggested

Discover 7 Scenic Hikes Near Calgary to Explore This Spring

Scientists Uncover Life’s Building Blocks in Ryugu Asteroid Samples

Windsor-Essex Unveils New Action Plan to Combat Substance Use

Boost Your Business Visibility with These Local SEO Strategies

East Algoma OPP Urges Public to Limit Travel Amid Hazardous Conditions

Universities Must Rethink Failure to Support Student Growth

Canada Invests $6.4 Million to Boost Green Shipping Corridors

Stony Plain Secures 14th Consecutive Award for Financial Reporting Excellence

Rhythm Pharmaceuticals Reports Strong Q4 Growth Ahead of FDA Decision

Brandon University’s Failed $5 Million Project Sparks Oversight Review

Microsoft Confirms U.S. Law Overrules Canadian Data Sovereignty

Winnipeg Celebrates Culinary Creativity During Le Burger Week 2025

New SĆIȺNEW̱ SṮEȽIṮḴEȽ Elementary Opens in Langford for 2025/2026 Year

EngineAI Unveils T800 Humanoid Robot, Setting New Industry Standards

Montreal’s Groupe Marcelle Leads Canadian Cosmetic Industry Growth

Tech Innovator Amandipp Singh Transforms Hiring for Disabled

Discover Aritzia’s Latest Fashion Trends: A Comprehensive Review

Dragon Ball: Sparking! Zero Launching on Switch and Switch 2 This November

Digg Relaunches as Founders Kevin Rose and Alexis Ohanian Join Forces

-

Education7 months ago

Education7 months agoBrandon University’s Failed $5 Million Project Sparks Oversight Review

-

Science7 months ago

Science7 months agoMicrosoft Confirms U.S. Law Overrules Canadian Data Sovereignty

-

Lifestyle7 months ago

Lifestyle7 months agoWinnipeg Celebrates Culinary Creativity During Le Burger Week 2025

-

Education7 months ago

Education7 months agoNew SĆIȺNEW̱ SṮEȽIṮḴEȽ Elementary Opens in Langford for 2025/2026 Year

-

Business4 months ago

Business4 months agoEngineAI Unveils T800 Humanoid Robot, Setting New Industry Standards

-

Health7 months ago

Health7 months agoMontreal’s Groupe Marcelle Leads Canadian Cosmetic Industry Growth

-

Science7 months ago

Science7 months agoTech Innovator Amandipp Singh Transforms Hiring for Disabled

-

Lifestyle3 months ago

Lifestyle3 months agoDiscover Aritzia’s Latest Fashion Trends: A Comprehensive Review

-

Technology7 months ago

Technology7 months agoDragon Ball: Sparking! Zero Launching on Switch and Switch 2 This November

-

Technology2 months ago

Technology2 months agoDigg Relaunches as Founders Kevin Rose and Alexis Ohanian Join Forces

-

Top Stories3 months ago

Top Stories3 months agoCanadiens Eye Elias Pettersson: What It Would Cost to Acquire Him

-

Health6 months ago

Health6 months agoEganville Leader to Close in 2026 After 123 Years of Reporting

-

Education7 months ago

Education7 months agoRed River College Launches New Programs to Address Industry Needs

-

Business6 months ago

Business6 months agoRocket Lab Reports Strong Q2 2025 Revenue Growth and Future Plans

-

Top Stories3 months ago

Top Stories3 months agoNicol Brothers Shine as Wheat Kings Dominate U18 AAA Hockey

-

Business7 months ago

Business7 months agoBNA Brewing to Open New Bowling Alley in Downtown Penticton

-

Education5 months ago

Education5 months agoAlberta Petition Aims to Redirect Funds from Private to Public Schools

-

Technology7 months ago

Technology7 months agoGoogle Pixel 10 Pro Fold Specs Unveiled Ahead of Launch

-

Technology6 months ago

Technology6 months agoDiscord Faces Serious Security Breach Affecting Millions

-

Education7 months ago

Education7 months agoAlberta Teachers’ Strike: Potential Impacts on Students and Families

-

Lifestyle2 weeks ago

Lifestyle2 weeks agoCanmore’s Le Fournil Bakery to Close After 14 Successful Years

-

Business7 months ago

Business7 months agoIconic Golden Lion Restaurant in South Surrey to Close After 50 Years

-

Science7 months ago

Science7 months agoChina’s Wukong Spacesuit Sets New Standard for AI in Space

-

Lifestyle5 months ago

Lifestyle5 months agoEdmonton’s Beloved Evolution Wonderlounge Closes, New Era Begins