Business

US Job Growth Expected to Remain Weak Ahead of Fed Meeting

US job growth is anticipated to remain subdued in September, with economists predicting an addition of only 50,000 jobs. This figure aligns with the average over the past three months, as the unemployment rate is expected to hold steady at 4.3%, which represents an almost four-year high. This lackluster performance highlights an ongoing sluggish trend in the labor market.

The upcoming report from the Bureau of Labor Statistics is scheduled for release on October 6, 2025. However, its publication is at risk if lawmakers fail to reach an agreement on a funding bill before the end of the fiscal year on October 1. A government shutdown would suspend federal economic reports, potentially delaying this key data.

Federal Reserve’s Interest Rate Decisions Uncertain

Should the report be released as planned, it will provide crucial insights for Federal Reserve policymakers regarding employers’ demand for labor. Recent cuts to interest rates were made this month in response to concerns about the fragility of the job market, marking the first reduction since 2025. Investors are now bracing for potential further cuts during the Fed’s upcoming two-day meeting, which concludes on October 29.

“Bloomberg Economics expects nonfarm payrolls for September to add a net 54,000 jobs. The improvement in net hiring likely came from leisure and hospitality, as temperate weather and a positive wealth effect from the summer stock-market rally drove spending on discretionary services.” — Anna Wong, Stuart Paul, Eliza Winger, Estelle Ou & Chris G. Collins, economists

As labor demand gradually diminishes, many companies are seeking strategies to offset rising costs, including higher import duties. Additionally, a separate government report is expected to show that August job openings were at one of the lowest levels since 2021, further indicating a cooling labor market.

Upcoming Economic Indicators and Global Context

In the coming week, the Institute for Supply Management will release its September surveys of manufacturers and service providers, which may provide further context regarding economic health. Investors remain alert for any last-minute developments ahead of the potential government shutdown, as these could have significant repercussions on economic stability.

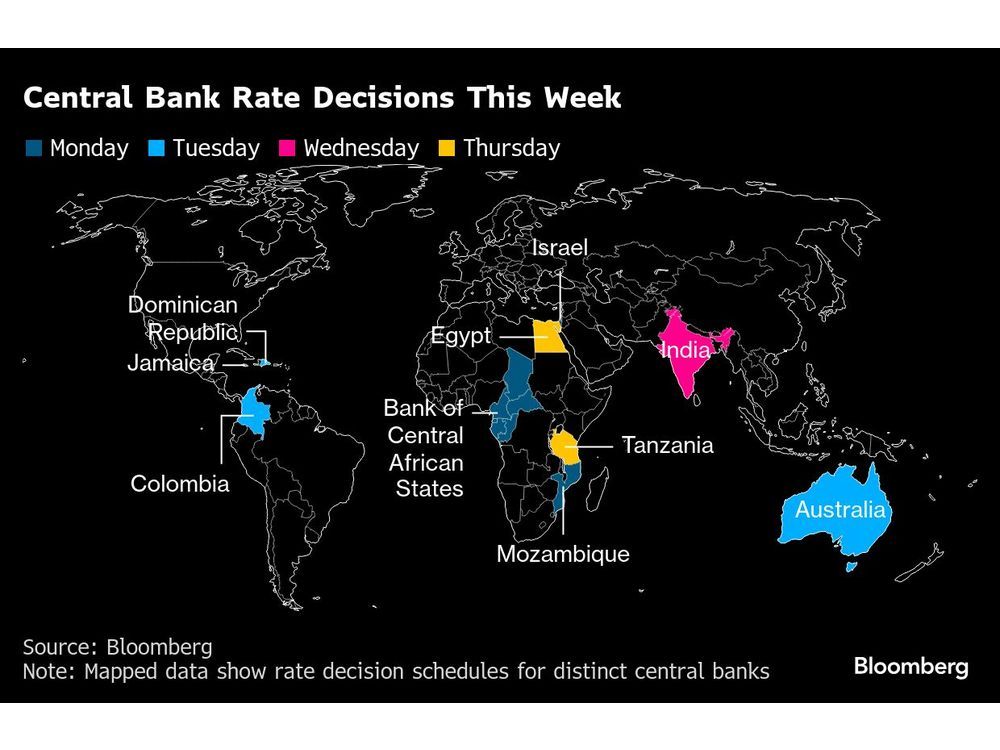

Global economic indicators will also be prominent. The Bank of Canada will release deliberations that led to its recent quarter-point rate cut, the first since March 2025. This may offer insights into future monetary policy decisions, particularly as markets consider the likelihood of another rate adjustment in October.

Across Europe, inflation data from multiple countries, including Spain, France, Germany, and Italy, will be released, shedding light on the overall economic climate in the eurozone. Forecasts suggest an inflation rate of 2.2%, the highest in five months.

As global central bankers convene to discuss monetary policy, attention will also focus on the Reserve Bank of Australia, which is expected to maintain its benchmark rate, and the Reserve Bank of India, which may lower its rate to 5.25%.

In summary, the upcoming job report and central bank meetings will be pivotal in shaping economic expectations both in the US and globally. Investors and policymakers alike will be keenly observing these developments as they navigate an uncertain economic landscape.

iShares Core Dividend Growth ETF Faces Challenges; Alternatives Suggested

Discover 7 Scenic Hikes Near Calgary to Explore This Spring

Scientists Uncover Life’s Building Blocks in Ryugu Asteroid Samples

Windsor-Essex Unveils New Action Plan to Combat Substance Use

Boost Your Business Visibility with These Local SEO Strategies

East Algoma OPP Urges Public to Limit Travel Amid Hazardous Conditions

Universities Must Rethink Failure to Support Student Growth

Canada Invests $6.4 Million to Boost Green Shipping Corridors

Stony Plain Secures 14th Consecutive Award for Financial Reporting Excellence

Rhythm Pharmaceuticals Reports Strong Q4 Growth Ahead of FDA Decision

Brandon University’s Failed $5 Million Project Sparks Oversight Review

Microsoft Confirms U.S. Law Overrules Canadian Data Sovereignty

Winnipeg Celebrates Culinary Creativity During Le Burger Week 2025

Discover Aritzia’s Latest Fashion Trends: A Comprehensive Review

New SĆIȺNEW̱ SṮEȽIṮḴEȽ Elementary Opens in Langford for 2025/2026 Year

EngineAI Unveils T800 Humanoid Robot, Setting New Industry Standards

Montreal’s Groupe Marcelle Leads Canadian Cosmetic Industry Growth

Tech Innovator Amandipp Singh Transforms Hiring for Disabled

Dragon Ball: Sparking! Zero Launching on Switch and Switch 2 This November

Digg Relaunches as Founders Kevin Rose and Alexis Ohanian Join Forces

-

Education7 months ago

Education7 months agoBrandon University’s Failed $5 Million Project Sparks Oversight Review

-

Science8 months ago

Science8 months agoMicrosoft Confirms U.S. Law Overrules Canadian Data Sovereignty

-

Lifestyle7 months ago

Lifestyle7 months agoWinnipeg Celebrates Culinary Creativity During Le Burger Week 2025

-

Lifestyle3 months ago

Lifestyle3 months agoDiscover Aritzia’s Latest Fashion Trends: A Comprehensive Review

-

Education7 months ago

Education7 months agoNew SĆIȺNEW̱ SṮEȽIṮḴEȽ Elementary Opens in Langford for 2025/2026 Year

-

Business4 months ago

Business4 months agoEngineAI Unveils T800 Humanoid Robot, Setting New Industry Standards

-

Health8 months ago

Health8 months agoMontreal’s Groupe Marcelle Leads Canadian Cosmetic Industry Growth

-

Science8 months ago

Science8 months agoTech Innovator Amandipp Singh Transforms Hiring for Disabled

-

Technology8 months ago

Technology8 months agoDragon Ball: Sparking! Zero Launching on Switch and Switch 2 This November

-

Technology3 months ago

Technology3 months agoDigg Relaunches as Founders Kevin Rose and Alexis Ohanian Join Forces

-

Top Stories4 months ago

Top Stories4 months agoCanadiens Eye Elias Pettersson: What It Would Cost to Acquire Him

-

Lifestyle3 weeks ago

Lifestyle3 weeks agoCanmore’s Le Fournil Bakery to Close After 14 Successful Years

-

Health6 months ago

Health6 months agoEganville Leader to Close in 2026 After 123 Years of Reporting

-

Education8 months ago

Education8 months agoRed River College Launches New Programs to Address Industry Needs

-

Top Stories4 months ago

Top Stories4 months agoNicol Brothers Shine as Wheat Kings Dominate U18 AAA Hockey

-

Business7 months ago

Business7 months agoRocket Lab Reports Strong Q2 2025 Revenue Growth and Future Plans

-

Business8 months ago

Business8 months agoBNA Brewing to Open New Bowling Alley in Downtown Penticton

-

Education6 months ago

Education6 months agoAlberta Petition Aims to Redirect Funds from Private to Public Schools

-

Education8 months ago

Education8 months agoAlberta Teachers’ Strike: Potential Impacts on Students and Families

-

Technology6 months ago

Technology6 months agoDiscord Faces Serious Security Breach Affecting Millions

-

Technology8 months ago

Technology8 months agoGoogle Pixel 10 Pro Fold Specs Unveiled Ahead of Launch

-

Lifestyle5 months ago

Lifestyle5 months agoEdmonton’s Beloved Evolution Wonderlounge Closes, New Era Begins

-

Business7 months ago

Business7 months agoIconic Golden Lion Restaurant in South Surrey to Close After 50 Years

-

Science8 months ago

Science8 months agoChina’s Wukong Spacesuit Sets New Standard for AI in Space